CBIC launched the MOOWR scheme to defer the Customs duties on imported goods that are used for the intended purposes of manufacture or carrying out other activities. The scheme is aimed at transforming India into a competitive manufacturing location and an attractive investment destination. Based upon Section 65 of the Customs Act, 1962, the scheme has clear and transparent procedures, simplified compliance requirements and digital account keeping.

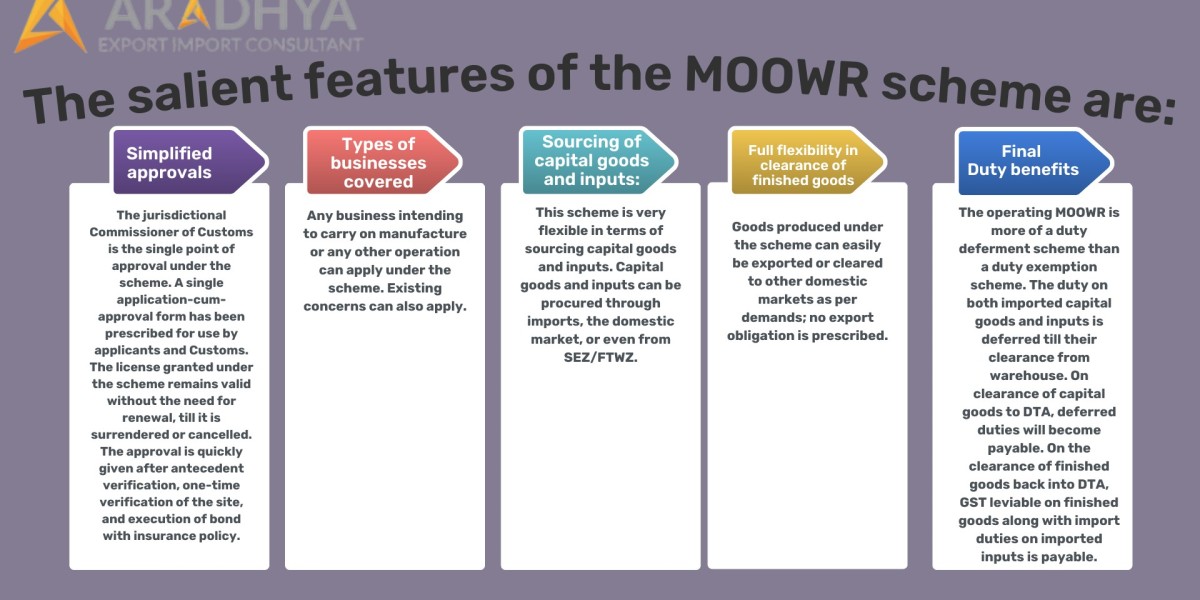

The salient features of the MOOWR scheme are:

1) Simplified approvals: The jurisdictional Commissioner of Customs is the single point of approval under the

scheme. A single application-cum-approval form has been prescribed for use by both the applicants and

Customs. The license granted under the scheme remains valid without the need for renewal, till it is

surrendered or cancelled. The approval is quickly given after antecedent verification, one-time verification of

the site, and execution of bond with insurance policy.

2) Types of businesses covered: Any business desiring to conduct manufacture or any other operations can apply

under the scheme. Existing businesses can also apply.

3) Sourcing of capital goods and inputs: The scheme gives flexibility in sourcing capital goods as well as inputs. The capital goods and inputs can be sourced through imports, domestic market or even from SEZ/ FTWZ.

4) Full flexibility in clearance of finished goods: The goods produced under the scheme can be exported or cleared to domestic market as per demand. No export obligation is prescribed.

5) Duty benefits: MOOWR is a duty deferment scheme and not a duty exemption scheme. The duty on both

imported capital goods and inputs stands deferred till their clearance from warehouse. In case of clearance

of capital goods to DTA, deferred duties will become payable. In case of clearance of finished goods into

DTA, GST on finished goods along with import duties on imported inputs are payable. The GST as well as the IGST paid as part of import duties will be available as credit. In case of export of capital goods or finished

goods, the duty on imported inputs stands remitted. Also, zero rating of tax on domestic inputs is allowed.